Active management (also called active investing) refers to a portfolio management strategy where the manager makes specific investments with the goal of outperforming an investment benchmark index.

Passive management (also called passive investing) is a financial strategy in which an investor (or a fund manager) invests in accordance with a pre-determined strategy that does not entail any forecasting (e.g. any use of market timing or stock picking would not qualify as passive management). The idea is to minimise investing fees and to avoid the adverse consequences of failing to correctly anticipate the future. The most popular method is to mimic the performance of an externally specified index.

Active vs Passive

There is a body of evidence which supports the rationale for index tracking (passive investing). One of the key drivers for the demand for active investment management is the investors seeking outperformance i.e. a return in excess of the return of the benchmark index it purports to outperform. Over the long term it is widely acknowledged that 97% of active fund managers fail to outperform the index. This is as a result of transaction costs; costs of expertise of the fund managers and the theory that markets are efficient. Certain niche markets may be less efficient and likely benefit from active fund managers as dealt with below.

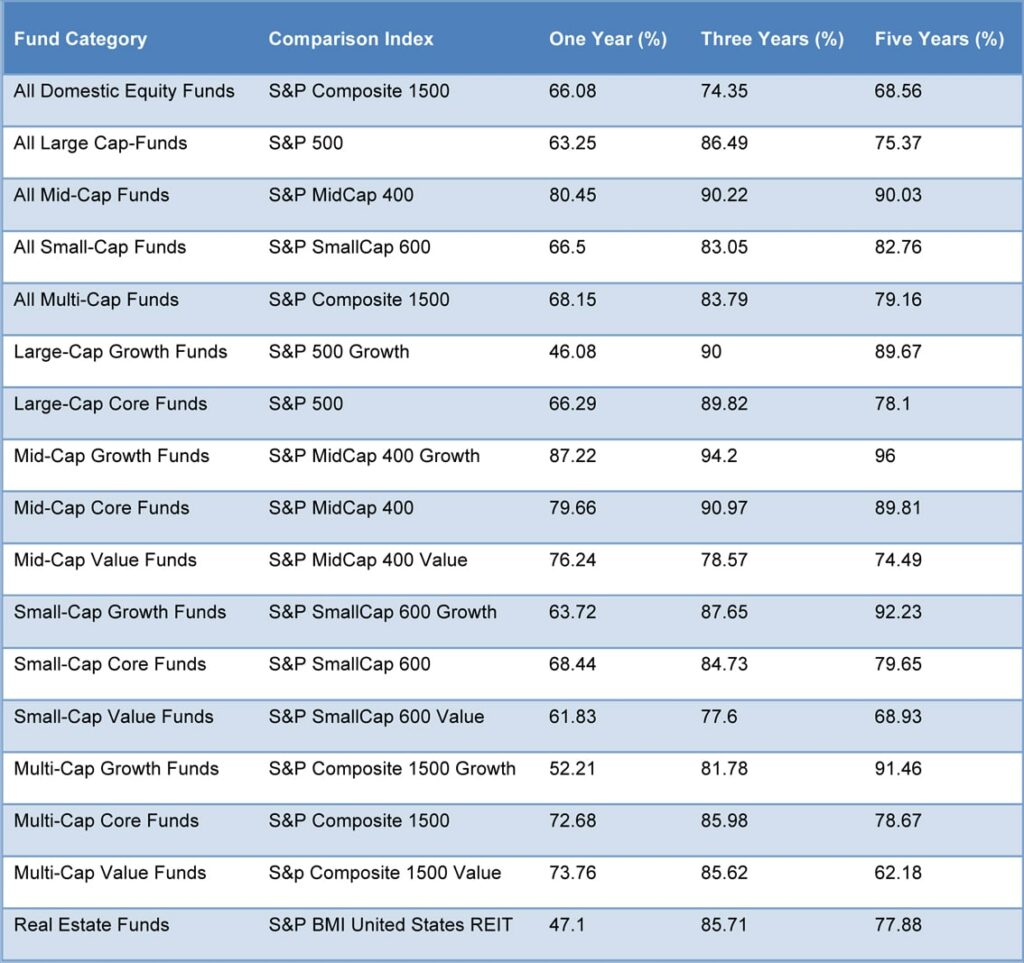

The table below demonstrates a 1, 3 and 5 year time frame of US Equity funds compared to benchmarks. This is an independent assessment called the SPIVA score card.

Efficient Market Hypothesis

Market efficiency says that prices reflect all available information and thus provide accurate signals for allocating resources to their most productive uses.

- All asset pricing models assume that Markets are efficient.

- Accordingly all available information in the market place is the driving force of setting market prices.

- If the efficient market hypothesis holds true there is little leverage for a fund manager; regardless of his expertise to manage the fund to consistently outperform the index.

- Of course there are defects in the efficient market hypothesis in specific instances and over shorter timeframes. However over an extended period of time the success of Active Fund managers who outperform the market index is as low as 3%.

- Developed markets which have high trading volumes tend to be the most informationally and operationally efficient. Less developed exchanges with lower volumes of trades arguably benefit the investor through active management.

- There is an argument to suggest that a specialist fund manager in a less developed market (such as emerging market funds) can add value.

- Similarly a fund manager deploying a specific investment strategy (such as absolute returns funds) may through strategic asset management add value.

- However BCWM views active fund management as a higher risk strategy than its passively managed counterparts because there is a 97% risk of underperformance.

An investor may be sceptical of the efficient market hypothesis concept or may despite the statistics wish to seek outperformance of benchmark indices for a portion of their investible wealth. In that instance an investor is faced with the decision of selecting an appropriate fund manager.

Although we believe that the broad based portfolio strategy should adopt a passive investment approach for equities and certain alternative varying yield investments which means that the investments will track a series of specified indices with the objective of matching market performance. The reason for the passive approach is to minimise risk by minimising the volatility and variability of returns relative to the index. Funds that track the index invest in shares in the constituent companies pro rata with the index.

Defects in Corporate Debt Index Tracking (passive) Model

Conversely, there is a strong argument to adopt the opposite approach for debt instruments. The nature of the corporate bond index is such that it is comprised of companies with the largest bonds, that is debt, in issue. Accordingly, by its nature the investee companies are highly leveraged. Therefore BCWM suggests using a series of strategic actively managed bond funds which will give the investor the exposure to bonds without the incremental risks posed by tracking the index.